By Jennifer Choe and Susan Cornett

Listen to a podcast-style summary of this blog post

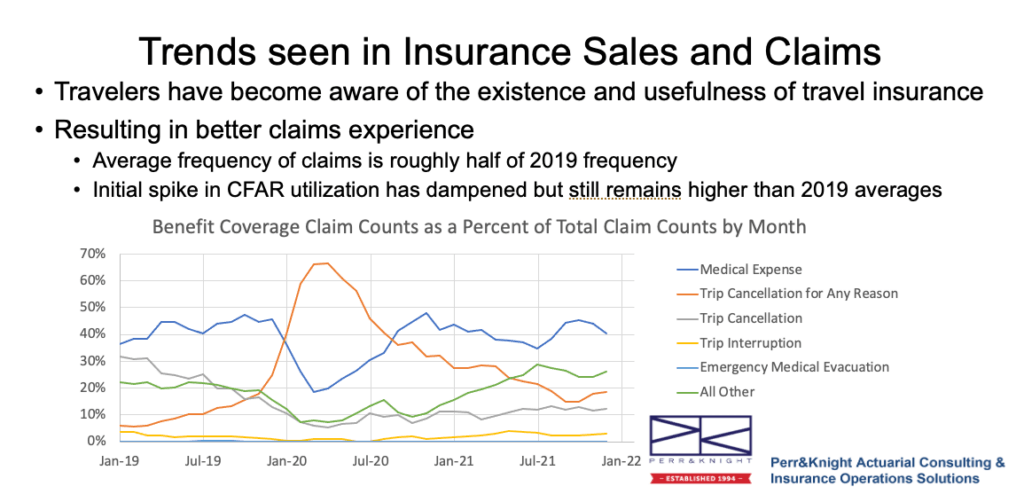

The backdrop: the travel insurance market is evolving

Travel insurance financial performance is shaped as much by policy language as by external events. Subtle drafting decisions around covered reasons, exclusions, and optional coverages can have a significant impact on claim frequency, severity, and rate adequacy.

As global travel returns to–or exceeds–pre-pandemic levels, there are many opportunities for insurance companies to offer products to a market that is hungry for options and more aware than ever of travel-related uncertainty. That said, increased volatility in today’s travel risk environment means insurance companies are under greater strain to achieve rate adequacy. Adding in competitors who are also looking to capitalize creates more demand on insurers to enhance benefits. This multi-pronged pressure cooker results in squeezed margins and sensitivity to loss ratio shifts that can affect profitability.

Decades of insurance product development and actuarial consulting for travel insurance have revealed how language can support or hinder speedy product approvals and long-term viability. Here are some ways your policy language can help you design competitive, defensible, and financially sustainable travel products.

Language defines the risk profile

Policy language plays a significant role in creating or limiting exposure. Unlike health insurance, for example, where policy language is extremely well defined, the gray area associated with travel insurance can be a buoy or an anchor on loss ratios, often in ways that aren’t evident until the policy is already in effect.

Some common examples of new or state-specific regulatory requirements include covered reasons definitions (e.g., supplier default, government travel advisories, weather-related cancellations), emergency medical evacuation definitions (including caps and sub-limits), pre-existing condition provisions (e.g., lookback periods, waiver language), and optional coverages like Cancel for Any Reason.

Insurers may often look for ways to make their products stand out, usually with the addition of new perils. These additions can change the underlying risk profile and require careful alignment with actuarial pricing assumptions.

Excess vs. first-dollar

In addition to properly defining policy language, another challenge for travel insurance, specifically travel medical benefits, most policies have the option to offer either primary or excess coverage, with most insurers choosing to offer excess coverage. However, some states do not permit travel medical benefits as excess, instead requiring that the policy pay first-dollar in the event of a claim. This requirement can be cost-prohibitive. “Excess vs. first-dollar” coverage is a foundational issue facilitating a significant impact on rates. While this first-dollar requirement cannot be changed, the rest of the policy language can be shaped to offset some of this risk.

Language changes are actuarial events

The product development process, specifically for travel insurance should incorporate actuarial consulting because small language adjustments can yield exponential results. Nebulous or undefined language can negatively affect claim frequency, claim severity, anti-selection risk, sensitivity to participation assumptions, and the risk that experience will differ from modeled scenarios. In short, a lack of clarity adds another layer of risk to travel insurance product development.

Pitfalls to avoid

Over the course of years of experience providing insurance product development and actuarial consulting for travel insurance, we have identified the most common missteps that can lead to rate adequacy issues or delays in filing approvals.

- Pricing developed before forms are finalized, or late form revisions after pricing is complete

- Mismatch between actuarial memo and form language

- Language inconsistencies that lead to regulatory objections

- Filing revisions that delay the approval process

- Failure to align benefit design when using competitor-based pricing

Preventing these missteps during travel insurance product development will save time and lead to a successful travel product launch.

Actuarial expertise supports product profitability

Working with experienced actuaries with a strong background in travel insurance can help you navigate pricing challenges and develop a competitive, sustainable product.

Comprehensive rate support includes stress-testing of policy definitions against pricing assumptions as well as scenario-testing to provide confidence intervals on rate adequacy. Actuaries must ensure there is alignment between the actuarial memorandum and policy language. This actuarial rate support provides stakeholders with information crucial for the product’s profitability in the competitive travel insurance market.

Why the right language pays off

Taking the time to examine the details – state regulatory differences, language definitions, comprehensive lists of inclusions and exclusions – during product and rate development is necessary. Precise language leads to more predictable loss ratio performance, stronger rate filing defensibility, less reactive re-pricing, and a faster time to market. In fact, policy language can be the edge a company needs to design a product that outperforms competitors and remains profitable well into the future.

Contact Perr&Knight today to learn more about our actuarial consulting services for travel insurance product development.