A little over 100 years ago the steel, oil & gas, and mining industries represented over half of the assets of the top 50 largest companies in the United States. Companies such as U.S. Steel, American Telephone & Telegraph (AT&T), Standard Oil, and Bethlehem Steel dominated the corporate world. What made these companies unique and valuable was that they were large manufacturing entities that owned hard assets such plants, machinery, inventory, storage facilities, phone lines, etc. These companies sought insurance coverage to protect these hard assets in the form of traditional insurance coverages such as commercial property, inland marine, machinery/equipment, etc.

Fast forward 50 years and industries such as technology, telecom, and film, along with oil & gas, now make up over 50 percent of the assets of the top 50 largest companies in the US. It’s also the first time companies in the medical industry have begun to make their way onto this list. Another shift takes place when the assets of these large companies start to become ‘softer’. Intellectual property begins to make its way onto the balance sheets of these larger firms. The film and medical industries were largely able to protect their assets through copyright and patent laws. Additionally, most telecom and technology firms still manufactured hard assets such as computers and phone lines. As such, the insurance industry remained largely unchanged in the coverages that were offered.

After the turn of the millennium, there is a significant change in the makeup of the top 50 list. The largest industries are now led by technology, financial services, and medical companies. Interestingly, the steel industry, which was by far the dominant industry in the early 1900s does not have a single company in the top 50. Now, five out of the top six firms are technology companies, but unlike their predecessors, today’s tech companies’ main assets include intellectual property such as software and data; otherwise known as digital assets. A digital asset is anything that is stored digitally and is uniquely identifiable that organizations can use to realize value. Examples of digital assets include consumer data, documents, audio, videos, logos, slide presentations, spreadsheets, and websites.

Unfortunately, the insurance industry hasn’t caught up with the ever-changing landscape of protecting companies’ digital assets. Crime coverage protects assets that are held by a custodian or investor, while cyber insurance covers first-party losses and third-party liability associated with system failure events, network security, and data privacy. However, most of these policies do not cover the actual loss of data or access to the data. For companies looking for coverage in the emerging digital asset space, it can be challenging to find reasonable insurance capacity at affordable pricing.

At Perr&Knight, our insurance product development experts have designed, developed, and supported numerous products for unique and debutant industries. Our clients have received approvals and started writing numerous products in practically all states. We can assist with actuarial rate and rule development, as well as drafting and reviewing policy language. We also offer compliance services such as licensing and filing work. If you are thinking of expanding into offering a digital asset protection program, please contact us today to discuss your strategy.

The digital asset insurance world is still uncharted territory with a lot of work to be done. However, if you take your time and proceed carefully, you’ll be in the best position to break in early to this market opportunity. Refer to our “From Concept to Reality” brochure for tips on navigating the successful launch of your new insurance products.

Insurance carriers have become more and more interested in writing “program” business over the recent years. In addition, many carriers only have a single carrier to work with, at least at the onset. Every carrier writing program business wants to have as much flexibility as possible to continue to add new programs and program administrators. Based on the experience of our actuarial consulting and state filings experts with various Departments of Insurance (“DOIs”) across the majority of lines, we describe below the most efficient way to set up nationwide filings and minimize the possibility of material compliance concerns.

What is program business?

According to the Target Markets Program Administrators Association, Program Business is defined as insurance products targeted to a niche market or class, generally representing a book of similar risks placed with one carrier. The administration of the program is done through Program Specialists, often referred to as program administrators or managing general agents (“MGAs”), who have developed expertise in that market or class. Although administrative responsibilities are negotiated between the Program Specialist and carrier, the responsibilities of the Program Specialist include underwriting selection, binding, issuing, billing, and oftentimes marketing, premium collections, data gathering, and claims management/loss control.

Bureau “Base” Program Filings

For the standard commercial lines, program business typically uses Insurance Services Office (“ISO”) or other rating bureaus for loss cost/rates, rules, and forms, but program business can be more than the standard commercial lines and can span across almost all Property & Casualty lines of business.

Some carriers choose to set up a “Base” program (usually for commercial lines) that any program administrator can use. For example, a Base program, such as commercial general liability, might adopt all the bureau loss costs, rules, and forms. There is no need to make a filing that is specific to a single program administrator or target market/class of business. This gives the program administrator the ability to start writing immediately rather than waiting for program filings to be prepared, submitted, and approved for their specific program.

According to our actuarial consulting experts, the Base program generally has rating flexibilities such as multi-tiering and a schedule rating plan, so the carrier can appropriately price the various markets and classes of business written by the carrier’s program administrators. If there are specific rates and forms that are required for a target market or class of business, the carrier will prepare and submit filings for these program-specific rates and forms. Generally, these are miscellaneous items that can be added on to the Base program and are simpler / quicker from a state filings standpoint compared to one with a complete program.

One of the drawbacks of the Base program filing approach is that changes have the potential to impact all program business. If a carrier is adopting an ISO loss cost change, one of their program administrators may not want to adopt the loss cost because of the impact on their specific niche market. Under this scenario, the carrier may file an exception in the Base program and carve out this specific market by having independent loss cost or rates for the impacted class of business. For the Base program approach, every time the carrier is filing a change to the Base program, they need to assess the impact on all their program business.

Program Business Filings

Rather than have all the program administrators use the same Base program filing, a carrier may elect to file each program separately. If a carrier chooses to also file a Base program, the program business filings are typically underneath the main Base program. This means that eligible risks are written in the program business filings and other risk are written in the Base program. The program business filings and the Base program filing are independent of each other in terms of bureau loss cost, rules, forms and company exceptions. When carriers have program business filings, they generally give the program business filing a special program name, like “Small Contractors Program”, with distinct eligibility guides to distinguish it from other programs the carrier may already have in place.

Under the program business filing approach, new program filings (rates, rules and forms) are needed for each new program administrator and it takes longer to get the program to market. However, our actuarial consulting experts have stated that structuring it this way makes the process much cleaner for rate revisions and program changes as no program filing is connected in any way to another under the same line of business.

Having your program filings connected to the Base program, although it can be done, generally causes issues. First off, many DOIs do not permit references (or links) to another program which makes tracking of these “links”, and lack thereof, difficult from a compliance perspective. In addition, if you make a change to the Base program, it could impact all linked programs which could potentially result in the same drawback mentioned for Base program and the change may not be desired by all program administrators.

Concerns with overlapping programs

Based on the experience of our actuarial consulting experts, multiple states have issues with a single carrier having multiple programs under the same line of business that could potentially offer the same insured different premiums for the exact same coverage. Many times the argument is made that these “programs” are independently run by separate management teams, so there is no insurance offering to the same insured by the same individuals. This argument does not always work and is problematic in California along with some other states. In addition, there are some states, such as California, that take this one step further in that no program can overlap within an entire insurance group, not just the individual carrier. When writing multiple programs for the same line of business under a single carrier, there are typically a few ways to differentiate programs in order to not run into state filing issues, which include the below.

Mutually exclusive underwriting guidelines

You are permitted to have multiples programs in all states if the underwriting guidelines are mutually exclusive, meaning no exposure overlaps between any approved program. For example, you could have a long haul trucking commercial auto program and a public auto commercial program, or from a personal lines standpoint, you could have one program that requires a usage-based insurance (“UBI”) device connected to the vehicle that tracks mileage, speed, breaking, etc. which impacts the driver’s premium and a regular program that does not have a UBI device requirement.

Material mandatory coverage differences

Multiple programs with similar exposures may be allowed to the extent that the programs have material mandatory coverage differences. For example, you could have an HO-5 (Comprehensive Form) homeowners program and an HO-3 (Special Form) homeowners program, since an HO-5 program is meant to be more expensive because the policy form is much broader than the HO-3 policy form. Issues can arise if the HO-5 premium is lower than HO-3 for the same risk. Additionally, if an applicant is eligible for both programs, the carrier must make both programs available to the applicant.

Different Distribution channels

Carriers may use distribution channels to differentiate programs, which include commission-based programs written by independent or captive agents and direct programs, with no commission, which are often sold on the internet.

Multiple Carriers

If an insurance group has more than one admitted carrier, the same, or similar programs can be filed under each carrier with none of the above issues occurring, except in a few states, based on our state filings experience. As was mentioned above, there are some states that look at the entire insurance group, not just the carrier.

Workers Compensation Issues

This line of business is different than other lines. In most states, due to statutory or other requirements, carriers may only have one program and must offer the same rates to everyone for standard (guaranteed cost) business. Therefore, a carrier that might have multiple commercial auto programs under the same carrier, can only have one program for workers compensation. In some jurisdictions, carriers can file to enhance the bureau rating structure, vary the rates offered within their single program, and individually rate certain qualifying risks.

Do you need guidance on maximizing the number of programs you can write under a single carrier in your personal or commercial lines rating plans? Our actuarial consulting and state filings experts at Perr&Knight are here to help.

The travel landscape has shifted dramatically over the past two years. From travel disruptions resulting from coronavirus variants to the recent surge in gas prices to the abrupt decline in both travel insurance sales and claims, it’s been a wild ride for travelers and insurance companies alike.

Here’s what has changed in the travel market over the last two years, how these changes have influenced today’s travel insurance product development, and what we expect to see moving forward.

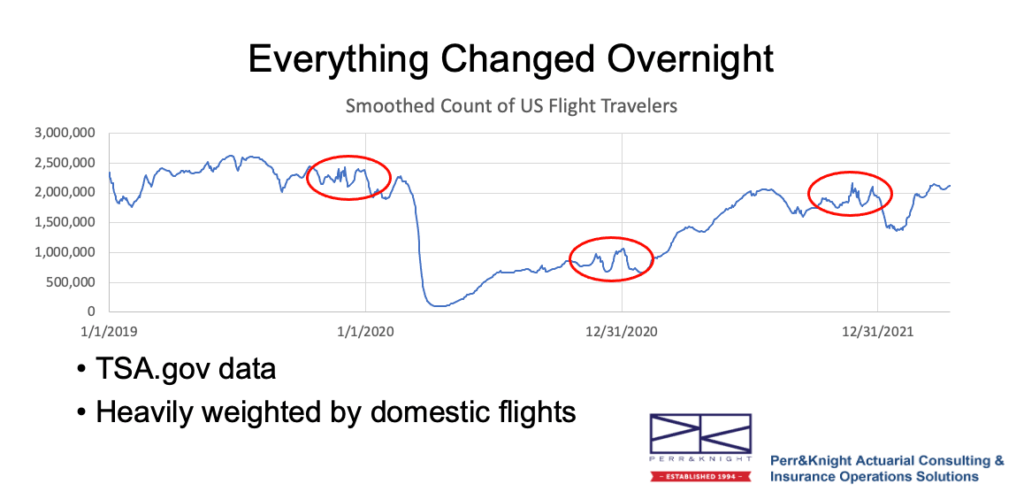

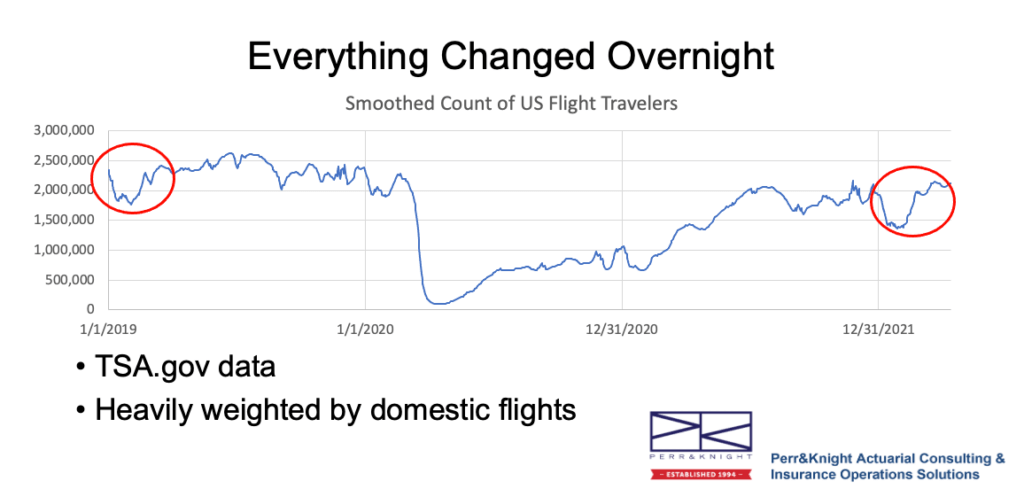

Flights as a measure of travel insurance health

Looking specifically at the number of flight bookings is the biggest indicator of what’s happening in the travel market today. Flights are a key indicator because historically, travel insurance was purchased more often when a flight was involved.

In 2019, we saw 2.5 million travelers a day pass through TSA. The initial landfall of Covid-19 in March 2020 threw the market into near-instant havoc, experiencing a sharp decline seemingly overnight. Since then, the travel industry has shown great strides in rebounding.

What’s important about today’s counts is the behavior or seasonality characteristics noted at the end of the year (“holiday season”) that mimic pre-pandemic travel, except at a lower level. However, Americans’ appetite for travel is gaining momentum quickly, resulting in numbers that are nearly back to 2019 levels in two short years.

We are also seeing similar travel behavior from 2019 mimicked in the first four months of 2022—further proof that the market has a strong foothold on the path back to “normalcy.”

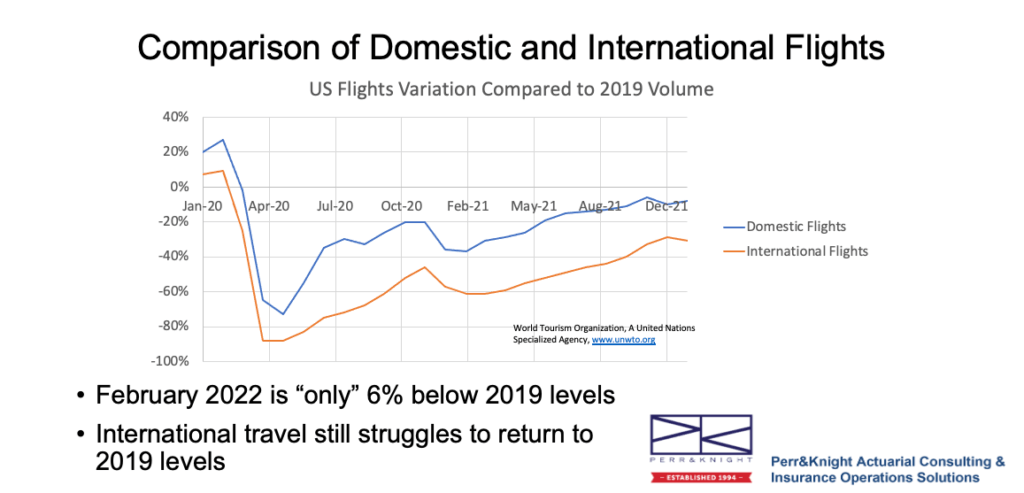

Flights and cruises are on the rebound

Beginning in 2020, the largest dip in travel behavior was due to the onset of Covid-19 first reaching the United States. Since that initial bottoming out, the market has made increasing trends upward. Domestic travel has started to gain momentum and is increasing at a rapid pace. As of March 2022, U.S. travel is only roughly 5% below 2019 levels, which is heavily weighted toward domestic travel. International travel experienced a more sluggish rebound in 2020 but is strengthening at nearly the same rate as domestic travel in 2021.

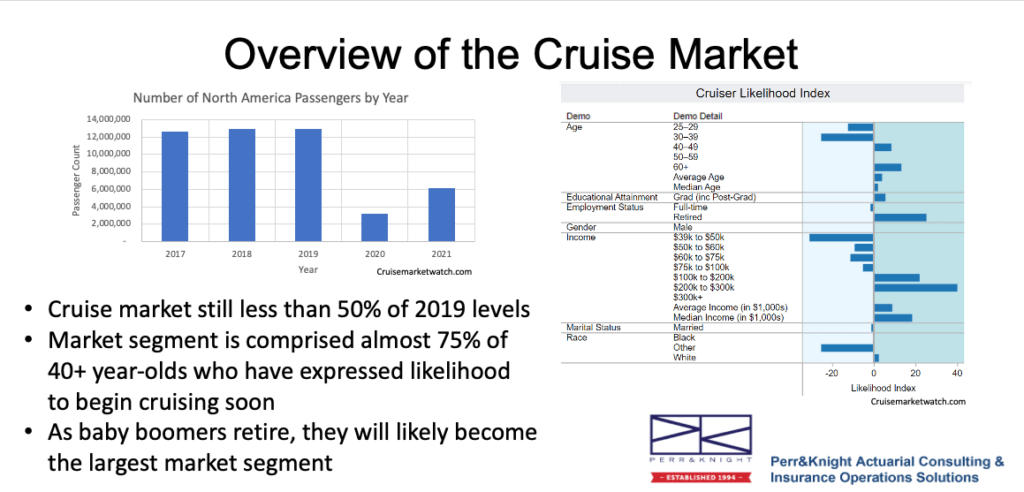

The cruising market took a near-instant nosedive once the outbreak of Covid-19 reached the United States. Today, cruising travel is still less than 50% of 2019 levels. During 2021, the cruising market has shown gradual (but slow) growth. Younger travelers are wary of the potential for virus transmission in enclosed spaces and are therefore not eager to board a ship anytime soon. However, older travelers appear to have a high likelihood to start cruising again soon. This is especially good news since the last of the baby boomers are reaching retirement age, meaning they have ample time and money for travel.

More travelers are hitting the road

Increased road travel is altering insurance product development to accommodate travelers’ changing needs. Travel by car and RV is having its day in the sun. According to the U.S. Travel Association, RV or car trips jumped in popularity in 2020 and 2021— a trend that appears to be continuing in 2022. Great news for the industry: 85% of Americans are expecting to travel this summer. Roughly 80% plan to travel in their personal or rental vehicles and 46% plan to fly.

Today’s travel insurance product offerings have been modified to focus on needs specific to road travelers, including medical coverage and rental car collision, as opposed to air travel-centric products like trip cancellation/interruption, missed flights, or lost baggage.

That said, 59% of American travelers believe travel prices are too high right now which has prevented them from traveling in the past month. The travel price index is 16% higher than 2019 levels, mostly due to rising fuel costs. However, this statistic does not indicate declines in future outlooks.

From pandemic to endemic: how coverage is changing

Many carriers considered pandemics like Covid-19 to be foreseeable events, so travel products have historically excluded events such as pandemics and epidemics. As a result, there was immense confusion among policyholders and insurance companies regarding specific coverages and exclusions for insureds who purchased travel insurance both before and after the initial outbreak of the virus.

That said, carriers continued to cover trip cancellation and trip interruption as well as medical expenses and emergency evacuation if an insured became ill, even due to the coronavirus.

As the virus moves from pandemic (actively spreading across borders) to endemic (a constant presence), insurance carriers are adjusting their insurance product development to reflect the “new normal” in the travel industry.

CFAR/IFAR

Policies generally do not cover cancellations or interruptions based on fear of contracting the virus, which is why “cancel for any reason” (CFAR) became such a hot topic. CFAR or IFAR (interruption for any reason) covers the cancellation or interruption of a trip under any circumstance. Even if the insured simply doesn’t feel like going on the trip anymore. Insureds who purchased this “any reason” benefit are covered and could recoup at least a portion of their trip. These benefits have since become a very sought-after benefit by insureds seeking peace of mind, which is especially relevant in case a new Covid-19 variant is detected.

Carriers are also reassessing pandemic and epidemic exclusions, opting to include them as covered perils in their policies. This is especially important as insureds start to take a closer look at their policies to determine what is covered and what isn’t.

Government-issued travel advisories

One of the coverages also being called into question today is trip cancellation or interruption due to government restrictions based on the U.S Department of State travel advisories. While cancellation or interruption may not cover the pandemic in general, cancellation or interruption because of government restrictions or travel advisories of level 4 (“Do not travel”) that could potentially include Covid-19 or various other reasons may be covered if the policy includes government restrictions as a listed peril in the policy. This may also include the CDC travel risk assessment of level 3 (“high risk”) which was recently revised and unveiled. Otherwise, government restrictions would not be covered. However, CFAR or IFAR would cover these scenarios.

Increased interest in travel insurance

Fortunately, the United States is essentially “back to normal” for domestic travel within the 50 states with no mandatory pre-arrival testing or quarantines. The federal mask mandate on commercial transit has also been discontinued. Vaccine and mask mandates are now based on state and city ordinances. The number of countries without travel restrictions also continues to climb as 2022 rolls on, which means the government restriction peril may no longer be as valuable as it once was.

A survey from the Automobile Club of America (AAA) found that one-third of U.S. travelers said they are more likely to buy travel insurance for their trips through the end of 2022, specifically because of the pandemic. 69% of travelers said, “the ability to cancel a trip and get a refund” is most important to them when considering travel insurance for an upcoming trip.

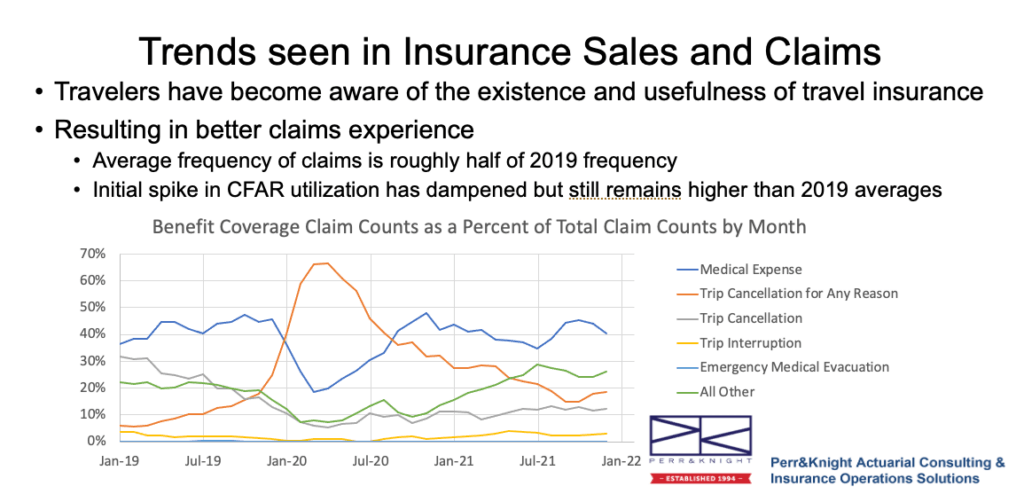

As more people become aware of the existence and usefulness of travel insurance, sales have seen a 10% to 20% jump over 2019 numbers with spikes as high as 53% increase over 2019 following news of the Omicron breakout. This increase in sales has resulted in a better claims experience than previously seen since anti-selection is being hedged against broader market sales.

The average frequency of 2021 claims based on internal data was less than half that in 2019. As a percent of total claims, the initial spike of CFAR claims has dampened but continues to be a highly utilized claim which we expect to continue into 2022, given consumers’ new knowledge about its value.

A new landscape

Covid-19 is here to stay. The initial fear of the virus is winding down, but the industry will continue to see spikes and dips as each new variant emerges. Travelers and insurers must learn to live with this new landscape and respond accordingly. Insurance companies must embrace this new landscape and take these shifts into account during their product development.

Another big takeaway for travel insurers is their ability to monitor claims. Claims submitted under CFAR should be categorized to determine those that are really for Covid-19 but may be disguised as something else. Tracking Covid-specific claims will help do just that. Likewise, more insurers have options specific to pandemic coverage and are providing coverage as its own benefit (trip cancellation, trip interruption, medical expense, and evacuations).

As consumers begin to feel more confident in their return to travel, the goal is to provide equal comfort in their protections through travel insurance.

Contact Perr&Knight and let our experienced actuaries and product design consultants help you develop insurance products that match today’s market.

On-demand insurance is a rapidly growing segment of the insurance market, providing policyholders with many benefits over the traditional insurance model. It can be purchased without directly interacting with a carrier representative, broker, or agent. While on-demand insurance is still new and a small segment of the insurance market, a study by Acumen Research and Consulting estimates the market to grow by nearly 30% by 2026 (1).

ADVANTAGES OVER TRADITIONAL INSURANCE

According to our insurance product development team, there are numerous advantages that on-demand insurance products have over traditional insurance:

Convenience: The application process for on-demand products is typically through a mobile or web application with an easy-to-understand interface, minimal number of questions, and the ability to tailor the coverage to a policyholder’s needs. Traditional insurance often involves lengthy interactions with carrier underwriters, agents, or brokers, which could involve protracted and complicated paperwork. More sophisticated on-demand products can obtain an applicant’s driving or claims history and auto-complete many data questions, further easing the application process for the customer.

Control: An on-demand policyholder can change the terms of their policy, add or remove coverages, and make other changes through their mobile or web application without having to make time-consuming and inconvenient calls to an underwriter, broker or agent. More sophisticated on-demand products provide many coverage customization options, putting powerful control of the coverage into the hands of the policyholder.

Instant Access: On-demand insurance coverage can be applied for and turned on in minutes. This is a big advantage in today’s economy where consumers are used to instant access (streamed music and video, same-day or one-day shipping, etc.).

Claims Handling: Claims can often be filed through a mobile or web application instead of having to contact a claims adjuster, adding further convenience and time savings.

Expense Savings: Commissions, brokerage costs, and other acquisition expenses are often lower due to the application process being handled through a mobile or web application. Automating the application and claims handling process can also lower the number of underwriters and claims adjusters needed and removes the need for additional paperwork. These costs savings can be passed onto the policyholders through lower premiums.

Usage and Need Based Coverage: Many on-demand products are offered on a short-term basis, from as short as one hour to several months, depending on when the policyholder needs coverage. Often, the policyholder can pause and then reactivate their policies to provide coverage only when they need it. Telematics allows for rating of auto insurance based on the actual miles driven. These features are important to gig economy workers who don’t need full coverage over an entire year, instead only needing coverages when they have a project or gig. Other examples of usage and need based coverages include travel or event insurance, with coverages purchased for a single trip or event.

Continuous Underwriting: Many on-demand products feature continuously updated pricing and risk profiles using real time data. Examples include usage base auto insurance using telematics, travel insurance using flight and weather data, and homeowners insurance using data from Internet of Things (IoT) devices.

Providing Coverage for Gaps in Insurance: On-demand insurance products can provide coverage for gaps in traditional insurance policies. For example, homeowners policies do not typically cover damages when a property is rented to others (Airbnb, Homestay). Personal auto policies don’t cover “business use” of covered vehicles. On demand insurance products can help provide coverages in both these instances and are especially suited to fill in these gaps on a usage and needs basis.

DISADVANTAGES OF ON-DEMAND INSURANCE

Of course, in our experience with insurance product development, we know there are also potential downsides and difficulties with products in this emerging market:

Moral Hazard: Since the application process is typically through a mobile or web application, it is difficult to audit the applicant responses for accuracy. Applicants can answer questions dishonestly in order to pay a cheaper premium. Insurers need to create better verification and auditing systems in order to ensure that risks are being priced appropriately.

Fraudulent Claims: Customers can potentially purchase on-demand coverage after the actual loss or damage has taken place and make a fraudulent claim that the damage took place after they turned on their coverage. Products that allow pausing and unpausing of coverages are especially susceptible to this risk.

Concentrated Exposure: On-demand policies will be purchased or turned on before a work shift or project so the exposure is highly concentrated for the policy term, in comparison to a standard annual policy that doesn’t allow pausing of coverage. Higher rates during usage should be charged to ensure that the premium collected adequately covers the concentrated risk.

Adverse Selection: Underwriting standards and knock-out questions are important for on-demand products. Less control over the underwriting process, with minimal ability to audit and review the applicant, can lead to riskier insureds being able to obtain on-demand coverage when they haven’t been able to obtain coverage in the standard market.

Regulatory Difficulties: On-demand programs have unique rating, form, and other program features that are different than the products that state insurance departments are used to reviewing. For example, short-term on-demand programs often file leveraged rating factors to provide higher premium for concentrated short-term coverages. Mobile and web applications require filing snapshots of each possible screen. Continuous and real-time pricing based on telematics, IoT devices or real-time travel data are difficult to support to the black-box nature of the technologies. This can result in a more difficult path to approval.

CURRENT ON-DEMAND PROGRAMS

Numerous on-demand insurance products are already available in many different lines of business, including:

Metromile offers personal auto coverage for a low monthly rate plus a per miles driven charge, tracked by telematics. Coverage can be switched on and off through the mobile application.

Thimble offers commercial general liability, miscellaneous professional liability, and inland marine coverages on a short-term, episodic basis. They allow their liability coverages to be paused and reactivated by the policyholders, through their mobile and web application. Thimble also provides coverage for drone/unmanned aerial vehicles liability insurance on an episodic basis. They have recently started offering episodic commercial property and event insurance in select states.

Cuuva is a United Kingdoms based insurer that offers personal auto insurance from 1 hour to 28 days in length.

Spot offers $20,000 of accidental injury coverage on a per month, subscription basis. This coverage can provided as a supplemental coverage to a traditional health insurance policy or can be the primary coverage for the roughly 30 million people without comprehensive healthcare coverage.

Flock provides drone/unmanned aerial vehicles liability and physical damage insurance coverage on an hourly, monthly, or per drone flight basis.

Surround offers Starter Pack insurance which includes bundled non-owned auto, renters, and miscellaneous professional liability coverage on a monthly basis, $60 per month. The products are designed for freelancers and other self-employed working professionals.

Digital Risks provides various business insurance coverages for small businesses, with a focus on digital assets, on an on-demand basis. Coverages are paid on a monthly basis. Available coverages include business owners insurance, professional liability and directors and officers liability.

Bind provides on-demand health insurance. The coverage options can be changed through the mobile application, including activating coverage during the year for less common, plannable treatments as needed.

Tapoly offers on-demand insurance coverage for small businesses, sole traders, freelancers, and the self-employed. Coverage options include professional liability, cyber liability, business owners property and liability, and directors and officers liability.

Duuo offers commercial general liability coverage on a daily basis, aimed at gig economy workers.

Authors: Mark Nawrath, PMP, MBA, and Dean Ferdico

Today’s technology advancements have the potential to transform businesses across industries. Aging systems and increased demand for new and innovative products mean insurance is ripe for disruption, but new solutions are not always as easy to implement as they may seem. Insurance is both complex and highly regulated: a double hit for Insurtech or non-insurance companies looking to break into the space. That said, there are endless opportunities for your company to make major waves in the industry…if you take a careful approach.

Based on our decades of insurance consulting along with our experience helping numerous Insurtech startups over the last several years, here’s what you should know as you break into the insurance market.

The insurance industry is highly regulated

Many of today’s Insurtech companies emerge from the finance world, where modern technology has transformed everything from customer service to the nature of banking itself. While U.S. banking must comply with a single federal charter, insurance products are subject to disparate rules in 51 jurisdictions, multiplied by 20 to 30 lines of business that each has its own individual coverages. The number of details required for each product filing can be staggering and small errors have the potential to stall the filing on the path-to-market.

Partnering with a seasoned insurance technology consulting company with state filings experts enables you to achieve a clear roadmap of what to expect, potential pitfalls, and areas to consider before you get too far along in the product development process. Experienced partners will provide you with a clear understanding of the playing field and help you draft a realistic strategy for rolling out your product.

Add insurance executives to your team

State Departments of Insurance (DOIs) look favorably upon companies with proven histories in insurance. They have no time to teach inexperienced technology companies or non-insurance companies the ins and outs of creating a compliant filing. Bringing a seasoned insurance executive onto your team – and partnering with proven insurance consultants – helps sidestep avoidable regulatory pitfalls and adds instant credibility to your organization in the eyes of the regulators. The same also applies when raising capital. Venture capital firms feel more comfortable investing in firms with experienced in-house teams and insurance consulting experts onboard.

Primary insurers are skittish

Around eight years ago, many primary insurance companies started issuing paper to unproven Insurtech companies – a move that ultimately damaged their standing with state DOIs. Since then, primary insurers (as well as reinsurance companies) are more discerning about with whom they will do business. After all, their reputations and licenses are on the line. This is where working with a seasoned insurance technology consulting company with state filings experts pays off. Having insurance consultants on your team to thoroughly review and pressure-test your proof of concept will help you stand out to primary insurers and reinsurance carriers.

Insurance compliance is full of hurdles

Receiving approval from state DOIs and remaining compliant also means your policy, billings, and claims administration systems must all meet regulatory standards. These standards include everything from how your products are priced to how you advertise to consumers to how data must be reported. Some requirement documents are thousands of pages long, a difficult task to manage for teams short on insurance experience.

Whether you are implementing an Insurtech solution or offering ancillary insurance along with your primary service offerings, insurance product development is a tricky process. Even bureau-based products that lean heavily on Insurance Services Office (ISO) or National Council on Compensation Insurance (NCCI) content are extremely complicated to interpret and adopt in a compliant manner. Seasoned insurance consultants like the team at Perr&Knight know this content and the related regulatory requirements inside and out because we work with them daily.

We help new Insurtech and non-insurance companies understand how to consume the content to develop an insurance product, how to structure the content for systems development and testing, and how to implement a compliant operational process from the outset. Building compliant systems and communications from the ground up protect your company from speed to market issues or costly re-work while avoiding potential fines for your carrier partner.

Use professional “matchmakers”

Primary insurance companies and reinsurers have what Insurtech companies and non-insurance companies need: approved licenses from state DOIs and capacity. Insurtech/non-insurance businesses have what primary carriers are looking for: fresh ideas, technologies, and access to new markets. Both must vet one another, a daunting task if neither company can accurately verify the validity of the other party’s credentials. Experienced insurance consultants like the team at Perr&Knight can provide an insurance-focused perspective to determine whether the partnership will be beneficial for both parties. Evaluations from unbiased insurance professionals can increase your confidence that your prospective partner can deliver.

The future is full of opportunity

Technology and consumer product development move with lightning speed. Insurance, on the other hand, is extremely sluggish. The merging of these complementary industries opens a plethora of opportunities for proactive companies, but success is never guaranteed. Re-framing your expectations, working with experts, and adopting a calculated approach to your new insurance offerings are the most effective ways to improve your position. Start exploring “what you know you don’t know” with seasoned insurance experts before you get too far down the road.

Here are some of the recent trends we’ve seen in accident & health coverage – and how insurance companies can respond more effectively to these changing times.

Younger consumers entering the market

The population of people purchasing insurance is shifting. This is a trend we have seen gain momentum over the previous few years with no sign of slowing down. More millennials (aged approximately 25-40) and Gen Z (age 24 and younger) consumers are buying insurance products. This shift in consumer base has a two-pronged effect: what products they seek, and how they are purchasing.

Older generations were content to work with a trusted insurance agent and prioritized a person-to-person relationship. Millennial and Gen Z consumers are more focused on instant information and instant gratification. Their digital-first consumption habits are causing insurance companies to re-evaluate how they offer products and are opening opportunities for Insurtech companies to fill the gap.

While Insurtech companies may have the technology covered, many have limited experience in the insurance space. Meanwhile, established insurance companies may have the knowledge of insurance product development but must partner with a technology provider to deliver products to consumers. Working with experienced insurance product development partners can help bridge the gap to make sure all products conform to regulatory standards.

The workforce is changing

As the gig economy continues going strong, more workers are tasked with securing coverage on their own. The federal insurance mandate is no longer in place, so consumers can be more creative with their health coverage. They want greater flexibility to choose plans and coverages that align with their needs and budget.

Some workers may not want or need full-blown health insurance plans, instead opting for more cost-effective coverages such as accident-only, major medical, critical illness, gap insurance coverage, or other supplemental plans.

Now is the time to revisit the scope of your medical products to determine if there are areas to offer products that align with today’s self-empowered purchaser. Insurance product development experts like Perr&Knight can provide insight into correct pricing and assist with rate and forms filings to bring these products to market as quickly as possible.

Short-term accident products

More and more insurance companies are offering lifestyle-related products that cover insureds under specific conditions for short periods of time. We’re seeing companies develop medical expense or accident indemnity products related to adventure sports, certain vacation activities, and equipment usage (ex. electric scooters).

Partner with insurance product development experts

Today’s trends unlock new possibilities for insurers to offer coverages that align with the times and evolving consumer expectations. However, everyone in the industry knows that product development, rate development, form filing, and approvals take time. Working with experienced actuaries and insurance product development specialists can accelerate your process and ensure you are not overlooking any critical elements that could slow your time to market.

At Perr&Knight, our insurance consultants help many clients develop group and individual supplemental health products. We are often approached by insurance companies with confusion about what group policyholder types to use and where a client should use group vs. blanket. When an employer policyholder is not appropriate, insurance companies look to other group types such as associations, trusts, or discretionary groups.

UNDERSTANDING GROUP POLICYHOLDER TYPES

Many clients want to rely on the outdated practice that, by using association or trust filings, a situs state approval means automatic approvals in other states and rating can be more flexible. While that was once the case, it no longer holds true. As associations became more popular, regulators noted that many of the associations lacked a common purpose and thought that the associations were used primarily to circumvent form and rate requirements.

Associations, trusts and discretionary groups often have to be approved by state regulators before a policy can be issued or, in some circumstances, before policy solicitation. Single case filings for these groups are required more often. Approvals for discretionary groups are particularly difficult to gain when the policyholder/insured relationship is not clear.

GROUP VERSUS BLANKET POLICIES

Another area of confusion is how a blanket policy is different from a group policy. On the surface they appear similar; there is a master policyholder and groups of individuals are covered. However, blanket coverage is usually offered to institutions (e.g. schools or camps) that provide excess or secondary accident/medical coverage to individuals participating in activities under their purview. While a few states require blanket coverage to have underlying certificates (like group), the people covered under these policies are often not aware that they have coverage under a blanket program.

HOW TO CHOOSE BETWEEN GROUP AND BLANKET POLICIES

Depending on the needs of the insurance company, policyholder and the individuals to be insured, insurance companies can utilize either a group or blanket policyholder format. Many jurisdiction handle non-employer groups and blanket programs differently. Some states will provide greater latitude to blanket products than group products simply due to the types of groups that may be insured.

Selecting a group type can be confusing so let our insurance consultants guide you. Our accident & health product development consulting team has ample experience in helping companies find success with non-employer groups.

There is no doubt that 2020 was a rough year in many respects. While the Coronavirus pandemic was frequently the topic of conversation, there was considerably more to talk about for those in the insurance industry.

According to a recent report published by the National Oceanic and Atmospheric Administration (NOAA), there were an unprecedented 22 extreme weather events in the United States last year, causing 262 fatalities and totaling at least $95 billion in damages. The previous record of 16 events was set in 2011 and matched again in 2017. By comparison, 2019 saw 14 extreme weather events with $45 billion in damages. While much of the country was under quarantine and stay-home advisories, others were ordered to evacuate for their safety. Many lives were changed after the disasters of 2020.

In late August, Hurricane Laura devastated the Gulf Coast and was the costliest event of the year with numerous fatalities and $19 billion in losses. However, this was only one of the record-setting 30 named storms of the 2020 Atlantic hurricane season, 13 of which developed into hurricanes. According to NOAA, the average season will have 12 named storms, six of which will reach hurricane status. This was only the second time that the Greek alphabet was tapped since each of the 21 letters used in the standard naming convention was exhausted. The only other time this has occurred was during the historic 2005 hurricane season that brought Hurricanes Katrina, Rita, and Wilma.

In addition to hurricanes, wildfires and convective storms ravaged other parts of the country. With a severe drought impacting more than a dozen states, conditions were favorable for massive wildfires that consumed more than 10.2 million acres, mostly in California, Oregon, and Washington and caused $16.5 billion in damage. Severe convective storms also contributed to the number of catastrophes last year, including a massive derecho that swept across much of the country from South Dakota to Ohio, leaving $11 billion of damage in its wake.

With the multitude of perils that we are exposed to, being responsive to the market and nimble in the ever-changing insurance landscape is critical. Whether it be rate or coverage revisions or new insurance product introductions, we have the expertise and the resources to enable you to deliver that peace of mind to your customers.

So much of what we find new and exciting requires what we too often write off as outmoded.

Today’s insurance technology initiatives are increasingly motivated by our latest term of art, digital transformation. We love to throw those words around as if they represent some magical incantation that, when invoked, will produce brilliant solutions that lift us to otherwise unattainable competitive positions, as masterworks of art that evoke feelings of awe eons after their original creation.

Of course, we’ve been “digitally transforming” for decades. Setting aside the nineteenth-century innovations of Charles Babbage for a moment, modern “digital” computing is easily traced at least as far back as 1945 with the introduction of ENIAC, “the first programmable, general-purpose electronic digital computer”.[1] The intervening years have seen a remarkable explosion of computing power. Famously, the Apollo Guidance Computer (AGC) used to put men on the moon in 1969, with its 2 MHz CPU speed, had roughly the same computing power as a twenty-five year-old Nintendo Entertainment System (1.8 MHz). An old iPhone 4 (2010), with its 800 MHz CPU speed, outgunned the $32 million Cray 2 supercomputer (1985) by a factor of three (244 MHz).[2] And today’s iPhone 12 (2.99 GHz) and Sony PlayStation 5 (3.5 GHz) make those computing milestones seem quaint.

The growth in computing power, and therefore the number of practical applications that can be handled by affordable computers, has been astonishing. Indeed, it has made the aspirations of computer scientists who only dreamed about artificial intelligence and virtual reality just a few decades ago – dreams because they would require rooms full of very expensive hardware – available to the masses in tiny packages for very modest sums.

So it follows that today when we hear about insurers wishing to undertake digital transformation initiatives, we understand that their desire is to leverage today’s massive computing power to gain a competitive advantage. Otherwise, we’re simply talking about modernization, which was all the rage way, way back in 2015. Today’s initiatives have the far more ambitious goal of producing novel solutions, in the sense that competitors haven’t yet discovered – let alone adopted – them, and so they’re in a very real sense disruptive.

But disruption comes out of tolerance for mistakes. Disruption comes from having the wherewithal to experiment and fail repeatedly. Disruption comes from having the courage to engage in radically candid conversations laced with dissent and debate. So disruption can only happen if the company culture permits it to happen – an idea antithetical to an insurance company’s traditional mission, which is to avoid undue risk.

This frosty bit of insight begs an entirely different approach to insurance company operations that goes well beyond technology. Famously linear thinkers, insurance professionals have historically worked to place a price x on some risk y in anticipation of a positive return z. We press this button and that happens. Of course, this approach has turned out to be of dubious value, evidenced by the prevalence of combined ratios that exceed the century mark. Instead, a confluence of factors in a variety of dimensions conspire to destroy our bottom lines, if not our innocence: Geopolitics. The environment. Social movements. Generational sensibilities. Competitive moves. Regulatory constraints. Human psychology. Solar flares?! And yes, the rapid pace of technological change. After all, how popular was cyber insurance – arguably influenced by each of those factors – in 1950?

Woke (forgive me, but the term seems to work in this context, too) insurers have accepted this. And so their efforts are directed toward aggregating not just traditional datasets that populate rating algorithms or underwriting rules, but those many ancillary bits of information that influence risk selection and loss potential in a far more informed (read: non-linear) way. They utilize Big Data. They leverage artificial intelligence. They employ dedicated predictive analytics units. They automate routine operational processes. They invest in new technology. And they adopt change management programs to support those initiatives. That’s a long list of expensive undertakings for a smaller insurer. But that’s the world in which they have to compete.

Middle-tier regionals with relatively modest means must contend with tiny upstarts with tens of millions in capital investment unburdened by years of legacy operations on one end, and multi-billion dollar behemoths spinning off autonomous innovation centers on the other, for their share of the hundreds of billions of premium dollars blown skyward by the shattering of preconceived notions.

And so we arrive at the intersection of culture and technology, of art and science, of hard skills and soft skills. In an industry famously fixated on risk avoidance and profit margins, this juncture becomes an especially challenging moment in time. Indeed, a quick review of recent literature on disruption in the insurance industry makes scant mention of the behavioral changes that must accompany any radical innovation, both within an organization among its constituents and outside among its customers and suppliers.

The impact on many well-established insurers? InsureTech startups are eating their lunch. That is, unless those veteran organizations were prescient (and well-capitalized) enough to develop their own skunkworks, separate and apart from their core organizations in order to permit the risk-tolerant cultures found in their more nimble adversaries. That’s fine if you’re a major player, one of the billion-dollar insurers who can afford separately funded venture arms, or an agile start-up with fifty million smackers to burn. But what of the middle tier, those thousands of regional insurers vying for market share in the face of old threats (mainstays) and new (InsureTechs)?

The obvious answer is they need to think a little differently. With no discretionary trove of millions to casually deploy, the focus must be on manifesting beneficial change. And beneficial change begins with vision, culture, and leadership – not bits and bytes. Old wine in new bottles, you might say.

I’m not suggesting plastering office walls with poster-sized admonitions to “embrace change,” nor am I suggesting that beneficial change is a thing that happens if you hire the right consultants. I am suggesting, however, that with all of the marvels of technology available in the twenty-first century, it’s still people who matter most. It’s still paying attention to what motivates – inspires – every individual responsible for the welfare of the organizations in which they toil that separates leaders from laggards. And most importantly, it’s regularly respecting and acknowledging their contributions to ensure they stay focused and motivated, long after the paint is dry on that beautifully executed automation project.

Of course, standard “tactical” practices for operational improvements and technology deployments involving proven toolsets for workflow analysis, business process design, and technical project management are essential for a successful digital transformation initiative. But no amount of funding will replace the unbridled enthusiasm of a group of colleagues setting out to effect change for the better. It’s that enthusiasm and commitment that drive organizations to prosperity; it is rarely prosperity – and never technology – that drives individuals to become enthused if they’re not adequately engaged and committed to the work they do.

Contact Perr&Knight to support your digital transformation initiative with experienced project managers, business analysts, and process improvement experts well-versed in the ‘people part’ of transformation, who can assist with the requirements management, process redesign, and change management capabilities that are essential for any such project.

[1] Swaine, M. ENIAC. (n.d.). Britannica. Retrieved January 25, 2021 from https://www.britannica.com/technology/ENIAC [2] Routley, N. (2017, November 4). Visualizing the trillion-fold increase in computing power. Visual Capitalist. https://www.visualcapitalist.com/visualizing-trillion-fold-increase-computing-power/.

The market for workers’ compensation insurance has undergone a shift as large employers with more bargaining power recognize they can achieve a better financial position by obtaining coverage that more closely aligns the total cost with their unique risk factors. State Departments of Insurance (DOI) have approved a number of sophisticated loss-sensitive options for workers’ compensation insurance, further prompting insurance companies to develop programs like these in order to remain competitive.

Below we have provided an overview of large risk rating workers’ compensation products and how Perr&Knight can help you develop competitive plans with the best chance of approval.

Large Deductible Plans

Large deductible workers’ compensation plans provide the same coverage as guaranteed or fixed cost plans, but with higher deductibles, possibly leading to reduced costs for insureds. Deductibles for these plans generally start at $25,000 to $100,000 per occurrence and are ideal for large employers seeking to self-insure a portion of their workers’ compensation losses.

Given the insurer is typically required to pay claims as they occur and seek reimbursement from the policyholder for claims below the deductible amount, insurers will often require the insured to provide collateral to secure the claims in this layer. Some jurisdictions may require insurance carriers to hold collateral, and insurers often need to analyze each risk individually to determine the amount of collateral to collect. This is an instance where turning to experienced actuarial consultants is invaluable. Our expert teams can assist in determining how much collateral to hold, either by performing actuarial loss projections based on historical loss runs prior to the onset of the policy or performing a collateral evaluation over time to ascertain how losses and collateral needs have developed for a particular policyholder.

Our actuarial consultants can help you develop your large deductible program, provide guidance on the various premium threshold requirements and permissible deductible levels by jurisdiction, as well as meet other state-specific requirements when filing large deductible workers’ compensation programs.

Retrospective Rating Programs

Retrospective (also called “retro”) rating plans determine the final workers’ compensation premium by evaluating actual losses incurred during the policy period. Employers pay a certain premium upfront, but at set intervals after the policy expires, insurance companies evaluate actual losses versus what was originally expected. This can result in a premium refund to the insured if losses are better than expected and additional premium due if losses are worse than expected. These sophisticated plans can be helpful in controlling the final cost of an organization’s workers’ compensation program.

Because of their complexity, it is imperative to set retro programs up correctly from the outset. Perr&Knight’s actuarial consultants can assist in determining proper rating factors (expected loss ratios, the types of excess factors to file, other rating elements to file in various states, etc.), as well as determining if the state DOI will allow exceptions to bureau filed plans.

Large-Risk Alternative Rating Option (LRARO)

A provision commonly contained in retrospective rating plans, LRARO can be layered on top of other programs, enabling employers with a yearly estimated workers’ compensation premium exceeding a certain threshold to negotiate premiums with their insurance provider. With this rule on file, insurers can negotiate the rating factors and premium components involved in determining the final premium for their workers’ compensation coverage.

This option is permitted in most states, but filing requirements vary by jurisdiction. For example, some states have premium eligibility requirements which must be met before the insurance company may use this rating option.

We have deep experience in developing loss sensitive rating programs and filing LRARO rules to achieve exceptional rating flexibility. Our actuarial consultants understand important jurisdictional filing differences and can help you file this provision correctly.

Partner with Actuarial Experts

Sophisticated large risk rating programs add more complexity to an already complicated process. Our actuarial teams are profoundly experienced in the full scope of loss sensitive programs and can help with designing large risk workers’ compensation products including developing rating plans, defining rules, helping with endorsements, and ultimately managing state filings.

For insurance companies already offering loss sensitive workers’ compensation products, we can conduct reviews to determine if it is possible to enhance your product offerings, or conduct detailed competitive evaluations to make sure your program is in line with the market.